Impact of rise in Import duty by Govt.of USA on Indian economy & other countries..... To upgrade USA Economy, Mr. Donald Trump, President of USA, has made historical decision to increase an import read more

Impact of rise in Import duty by Govt.of USA on Indian economy & other countries.....

To upgrade USA Economy, Mr. Donald Trump, President of USA, has made historical decision to increase an import duty on aluminium & steel which are used mainly in Space and Automobile industries. With the implementation of new rates of import duties by USA Govt, professional activities on the ports & air terminals across the globe have slowed down and many countries have started cancellation of their confirmed orders. Industrial productions has also slowed down. This is the beginning of a trade war which was predicted by expert Economists. There is going to be a lot of pressure on the world economy and all the countries will end up paying very heavy price for this.

History says that Trade War has proved very fatal for the world economy as a whole as it increases enmity between various countries and there is a threat for the whole world coming under the influence of one single country..

This, in turn, is going to adversely affect Indian economy which in turn is going to affect all the professionals also.

COST AUDIT Section 148 of the Companies act 2013 provides the provision of Cost Audit and The Central Government issued Companies (Cost Records and Audit) Rules, 2014 on June 30, 2014. Government read more

COST AUDIT

Section

148 of the Companies act 2013 provides the provision of Cost Audit and The

Central Government issued Companies (Cost Records and Audit) Rules, 2014 on

June 30, 2014.

Government

needs authentic and reliable data of cost for various purposes like price

fixation of controlled commodities. The information is also useful in various

decisions like fixation of duty drawback, export incentives; amount of excise

duty the product can bear, deciding whether special incentives are required to

a particular industry etc.

There

are certain and rules have been provided for regulation and working of Cos

Audit.

Subsequently,

various amendments are carried out in the above rules as enumerated below from

time to time till date:

The Companies (Cost Records

and Audit) Amendment Rules, 2014 dated 31/12/2014

This amendment brought the

changes as pointed below:

i.

Definition of Central excise tariff heading given

ii.

Rule 3 – Application of cost records substituted – Table A and Table B added

iii.

Rule 4 – Applicability of cost audit substituted – Table A and Table referred

iv.

Proviso to Rule 5(1) inserted.

v.

Rule 6(3A) inserted – to give the provision to fill the casual vacancy within

30 days.

vi.

Rule 7 (Rules not to apply in certain cases) omitted

vii.

Form CRA-1 and CRA 3 substituted

2. The Companies (cost

records and audit) (Amendment) Rules, 2015 dated 12/06/2015

This amendment brought the

changes as pointed below:

i.

Amendment in CRA-2 & CRA-4

3. The Companies (cost

records and audit) (Amendment) Rules, 2015 dated 14/12/2015

This amendment brought the

changes as pointed below:

i.

Rule 13 of The Companies (Cost Records and Audit) Rules, 2014 was substituted

with new clause

4. The Companies (cost

records and audit) (Amendment) Rules, 2016 dated 14.07.2016

This amendment brought the

changes as pointed below:

i.

Definition of cost audit Report is substituted with the new one

ii.

Table A and Table B given under Rule 3 are substituted.

iii.

Rule 4(3)(iii) is inserted to include captive generation plant.

iv.

proviso to Rule 6 (1) written consent of the cost auditor is required to be

obtained.

v.

Rule 6(1A) inserted to include certificate from cost auditor in terms of

section 141

vi.

Proviso to Rule 6 (3) inserted for removal of cost auditor before expiry of

term.

vii.

Rule 6(3B) inserted to include approval of Board of directors for the cost

statements and annexures of cost audit report before signed on behalf of board.

viii.

Rule 6(5) substituted for providing that cost audit report shall be submitted

to board within 180 days from closure of FY.

ix.

Rule 6(6) substituted to provide filing of cost audit report in form CRA-4-XBRL

within 30 days of receipt

Section 148 of the

Companies Act, 2013 read with the Companies (Cost Records and Audit) Rules,

2014 (by considering various amendments as mentioned above) are applicable and

governs the maintenance of cost accounting records and cost audit

APPLICABILITY-

Every

company including a foreign company engaged in the production of goods or

providing services specified in the Tables -A & B of rule 3, having an

overall turnover from all its products and services of Rs 35 crores or more

during the immediately preceding financial year shall include cost records for

such products and services in their books of accounts maintained.

RULE-3

The Rule 3 has classified

sectors under Regulated and Non-Regulated sectors.

The

sectors covered under Table A are under the Regulated Sector and sectors

covered under Table B are under the Non-Regulated Sector.

Every

company engaged in the production of the goods or providing services, specified

in Tables (Table A – Regulated sectors and Table B – Non-regulated Sectors),

having an overall turnover from all its products and services of Rupees thirty

five crore or more during the immediately preceding financial year, shall

include cost records for such products or services in their books of account.

Provided

that nothing contained above shall apply to a company which is classified as

micro enterprise or a small enterprise including as per the turnover criteria

under sub-section (9) of section 7 of the Micro, Small and Medium Enterprises

Act, 2006.

RULE-4

Rule 4states that cost audit

would be applicable to a company if the classification of company falls under

Industry / Sector / Product / Service provided in Table A or Table B and:

For

any company to fall under the requirement of Cost Audit following two tests

shall apply:

a. Coverage under Table – A

and / or Table – B.

Company’s

product / services shall fall under one or more categories given under Table A

and / or Table B. AND the respective Central Excise Tariff Act (CETA) headings

(wherever applicable).

b. Turnover:

(i)

If the products or services of the company falls under Table A – Regulated

sectors:

Overall

annual turnover from all products and /or services is Rs. 50 crore or more AND

aggregate turnover from individual product or services for which cost records

are required to be maintained is Rs. 25 crore or more, during the immediately

preceding financial year;

(ii)

If the products or services of the company falls under Table B – Non-regulated

Sectors:Overall annual turnover from all products and / or services is Rs. 100

crore or more AND aggregate turnover from individual product or services for

which cost records are required to be maintained is Rs. 35 crore or more,

during the immediately preceding financial year.

Exemption from applicability

of Cost audit(Rule 7):

The

requirement of Cost Audit under these rules shall not apply to a company which

is covered in Rule 3, and –

i.

whose revenue from exports, in foreign exchange, exceeds 75% of its total

revenue; or

ii.

which is operating from a special economic zone.

RULE-5

MAINTAINANCE OF RECORDS

The

requirement to maintain cost records in Form CRA-1 have been postponed to

Financial Year 2015-16 for the following companies in some non-regulated

sectors, namely; Coffee and Tea, Milk Powder and Electricals and electronic

machinery.

Every

company, which comes under the Rules, including all units and branches, shall,

in each financial year from 1-4-2014, maintain cost records in Form CRA-1.

In

the case of company covered in serial number 12 (coffee and tea) and serial

numbers 24 to 32 of item B of Rule 3, the requirement of Rule 5 shall apply in

respect of each of its financial year on or after 2014-2015.

The

above cost records shall be maintained on regular basis so as to help

calculation of per unit cost of production or cost of operations, cost of sales

and margin for each product and activities for every financial year on monthly,

quarterly, half-yearly or annual basis.

The

cost records shall be maintained in such manner as to enable the company to

have control over various operations and costs to achieve optimum economies in

utilization.

RULE-6

Pursuant

to the rules 3 and 4, it is clear which are the companies to whom Cost Audit

shall be applicable in every financial year and therefore there is no need for

the Central Government to issue order directing Cost Audit.

Cost Audit Report-Rule 6(4)

as amended on 31-12-2014

The

Cost Auditor shall submit the Cost Audit Report along with his or its

reservations or qualifications, if any, in Form CRA-3 to the Board of Directors of the company within a

period of 180 days from the closure of the financial year.

The

Board of Directors shall consider and examine such report, particularly any

reservation or qualification contained therein.

The

cost statements, including other statements to be annexed to the cost audit

report, shall be approved by the Board of Directors before they are signed on

behalf of the Board by any of the director authorised by the Board, for

submission to the cost auditor to report thereon";

Copy of the Cost Audit Report

to be furnished to the Central Government:

Every

Company shall forward a copy of Audit Report to the Registrar of Companies

within 30 days of receipt of the Audit Report along with the full information

and explanation on every qualification or reservation, if any, in Form CRA-4with fees specified in

Companies (Registration Offices and Fees) Rules, 2014.

Duty of the Cost Auditor to

report on commission of offence found during the Audit-Rule 6(7)

In terms of Section 143(12) of the Act, if the

Cost Auditor, in the course of his duties as Cost Auditor, has reason to

believe that an offence involving fraud has been or is being committed against

the Company by its officers or employees, he shall immediately report the

manner to the Central Government.

Content of the Certificate of

cost Auditor:

The

individual or the firm, as the case may be, is eligible for appointment and is

not disqualified for appointment under the Act, the Cost and Works Accountants

Act, 1959 (23 of 1959) and the rules or regulations made thereunder.

The

individual or the firm, as the case may be, satisfies the criteria provided in

section 141 of the Act, so far as may be applicable.

The

proposed appointment is within the limits laid down by or under the authority

of the Act;

The

list of proceedings against the cost auditor or audit firm or any partner of

the audit firm pending with respect to professional matters of conduct, as

disclosed in the certificate, is true and correct.

APPOINTMENT OF COST

AUDITOR-

Who can be appointing as cost

auditor:

A

cost Accountant in practice or a firm of cost accountants can be appointed as a

cost auditor.

A

cost accountant holding certificate of practiced on part time basis is not

entitled to conduct cost audit. Thus, only a cost accountant in whole-time

practice can conduct cost audit.

Who can’t appoint as cost

auditor:

Statutory

Auditor appointed under Section 139 of the Act can’t be appointed as Cost

Auditor of the Company.

Process for appointment of

Cost Auditor:

Consent

of Auditor: Before appointment is made, the written consent of the cost auditor

to such appointment, and a certificate from him or it, as provided in sub-rule

(1A), shall be obtained.

If

Company has Audit Committee: Appointment and remuneration will be recommended

by audit committee and approved by Board.

If

Company doesn’t have Audit Committee: If there is not audit committee, appointment

and remuneration fixation will be done by Board. Later, this remuneration shall

be ratified by Shareholders.

Information for appointment

Cost Auditor:

a.

Information to Cost Auditor: Every Company which requires appointment of Cost

Auditor shall inform the Cost auditor of his appointment within 30 days of

Board Meeting in which resolution for appointment has passed.

b.

Information to ROC: Company will file

form CRA-2 with ROC: Within 30 days of passing of Resolution in Board Meeting,

OR Within 180 days of the commencement of financial year. Whichever is earlier.

Removal of Cost Auditor:

The

cost auditor appointed may be removed from his office before the expiry of his

term, through a board resolution after giving a reasonable opportunity of being

heard to the Cost Auditor and recording the reasons for such removal in

writing.

Appointment of Cost Auditor

in case of Casual Vacancy:

Any

casual vacancy in the office of a cost auditor whether due to resignation,

death or removal, shall be filed by the Board of Directors within 30 days of

such Vacancy.

Company

will file form CRA-2 with ROC within said 30 days. Period by which appointment

to be made-Rule 6(1): The concerned companies shall appoint the Cost Auditor

within 180 days of the commencement of every financial year.

Limit of number of Cost

Auditor:

Limit

of number of audit per person, as are applicable to Statutory Auditors are

applicable to Cost Auditors.

Qualifications, Rights,

Duties and obligations of Cost Auditor:

The

qualification, disqualification, rights, duties and obligations of Cost

Auditor/firm of Cost Auditor are same as applicable to Statutory Auditors.

Note: The auditor

conducting the cost audit shall comply with the cost auditing standards.

Punishment on

contravention of this Section:

To the company:

The

company shall be punishable with a fine which shall not be less than Rs.

250,00.00 but which may extend to Rs. 5,00,000.00. Every officer of the company

who is in default shall be punishable with imprisonment for a term which may

extend to 1 year or fine which shall not be less than Rs. 10,000.00 but which

may extend to Rs. 1,00,000.00 or with both.

To the auditor

He

shall be punishable with a fine which shall not be less than Rs. 25000.00 but

which may extend to Rs. 5,00,000.00. However, if the auditor has contravened

such provisions willfully with the intention to deceive the company or its

shareholders or creditors or tax authorities, he shall be punishable with

imprisonment for a term which may extend to one year and with fine which shall

not be less than Rs. 1,00,000.00 but which may extend to Rs. 25,00,000.00.

In

case the criminal liability of an audit firm, the liability other than fine

shall devolve only on the concerned partner who acted in fraudulent manner.

(A) Regulated Sectors

Sl.

No.

Industry/Sector/Product/Service

Central Excise

Tariff Act(CETA) Heading (wherever applicable)

1.

Telecommunication

services made available to users by means of any transmission or reception of

signs, signals, writing, images and sounds or intelligence of any nature and

regulated by the Telecom Regulatory Authority of India under the Telecom

Regulatory Authority of India Act, 1997 (24 of 1997); including activities

that requires authorization or license issued by the Department of

Telecommunications, Government of India under Indian Telegraph Act, 1885 (13

of 1885);

Not applicable

2.

Generation,

transmission, distribution and supply of electricity regulated by the

relevant regulatory body or authority under the Electricity Act, 2003 (36 of

2003);

Generation- 2716;

Other Activity-Not Applicable

3.

Petroleum

products; including activities regulated by the Petroleum and Natural Gas

Regulatory Board under the Petroleum and Natural Gas Regulatory Board Act,

2006 (19 of 2006)

2709 to 2715;

Other

Activity-Not Applicable

4.

Drugs and

pharmaceuticals

2901 to 2942; 3001

to 3006

5.

Fertilizers

3102 to 3105

6.

Sugar and

industrial alcohol

1701; 1703; 2207

(B) Non-Regulated Sectors

SI. No.

Industry/ Sector/

Product/ Service

Central Excise

Tariff Act Heading (wherever applicable)

1.

Machinery and

mechanical appliances used in defence, space and atomic energy sectors

excluding any ancillary item or items;

Explanation.

– For the purposes of this sub-clause, any company which is engaged in any

item or items supplied exclusively for use under this clause, shall be deemed

to be covered under these rules

It has been almost a year and half that the Insolvency & Bankruptcy Code ('Code') aimed at solving and easing out insolvency process was enacted. An unprecedented framework was established with this read more

It has been almost a year and half that the Insolvency & Bankruptcy Code ('Code') aimed at solving and easing out insolvency process was enacted. An unprecedented framework was established with this as the board of directors of the company was dissolved, a moratorium was effected, Committee of Creditors was made in-charge of the day-to-day affairs of the company and a new institution / profession of Resolution Professionals was established. The Code had strictly mandated that within 180 days (90 days as extension from the NCLT) the resolution process of an insolvent company had to be completed.

Since then, issues regarding the interpretations of the Code have kept the NCLT, the NCLAT and the Supreme Court busy as even the judiciary endeavoured to not disturb the pace of ongoing proceedings. The matters which came up extended from determining the meaning of term ‘dispute’ to disqualification of Resolution Applicants.

In wake of this, the first amendment to the Code was given effect in 2017 which introduced Section 29A prohibiting certain persons from submitting resolution plans. With rising complexities in the Code, the recommendations of the fourteen-member committee were considered for easing out the complexities. On 6th June 2018, giving effect to the recommendations, a second ordinance has been promulgated by the Union government for balancing the interests of various stakeholders, promoting resolution of corporate debtor and clarifying the provisions relating to eligibility of resolution applicants.

Key Amendments and Analysis

1. Homebuyers and Financial Creditors

The question regarding the status of home buyers was looming large since the time associations of home buyers made an application to stay insolvency resolution process of Jaypee Infratech before the Hon’ble Supreme Court. Their foremost grievance was related to their treatment as unsecured creditors of the company, as a result of which they were to be at great loss by incurring substantial haircuts on their amount to real estate companies coupled with the risk of losing their future homes. The Insolvency and Bankruptcy Board of India, in the meanwhile, had introduced Form F for home buyers to register their claims with the appointed resolution professional. The Supreme Court had taken a considerate stand for these home buyers in the cases regarding these real estate companies viz. Jaypee, Amrapali and Unitech.

This amendment was heavily critiqued earlier, however, has paved its way into the law of the land.

The amendment would be welcomed by homebuyers who were stranded in middle as they were also not able to pursue their remedies under the Consumer Protection Act, 1986 because of the moratorium imposed on the legal proceedings against the developer companies. As a result of the amendment, they will be treated at par with the lending institutions and their rights would be guaranteed before the operational creditors. This would make sure that the money deposited with the developer companies is substantially received back by them in case of insolvency.

On the other hand, this might be worrying for the banks and other lenders who form the Committee of Creditors. As, in the case of insolvency process, the Committee of Creditors is at the helm of affairs of the company and is constituted by the financial creditors, as an effect of the Ordinance the home buyers too will be part of this very Committee. Moreover, the homebuyers will also be holding voting power in proportion of the overall credit. Although, on an individual level the voting power would be negligible, the associations of such homebuyers would be having substantial voting power. Thus, it can be a cause of fear among lenders that during the resolution they might lose control of the process.

Earlier, the homebuyers had also their rights secured in the Consumer Protection Act, 1986 and the newly enacted Real Estate (Regulation and Development) Act, 2016. While under the former legislation the redressal forum was State Commission or National Commission, the latter authorised Adjudicating Officer under the RERA.

2. Relief for MSMEs

The amendment has removed the restriction of promoter not being eligible to participate in the bidding process with respect to the MSMEs. This measure was taken in the light of the fact that resolution process of such MSMEs did not attract others outside the scope of promoters. This would ensure that a resolution plan is made for these entities and are not just liquidated because of no bidders.

3. Reduction in voting threshold

As the intent behind the Code was always to revive the company and not to liquidate it, there were issues with regard to the higher voting requirement in the Committee of Creditors for passing resolutions. The amendment thus, has reduced the voting threshold from 75 per cent to 66 per cent for instances such as passing the resolution plan. Also, for regular functioning too 51 per cent is now the threshold.

4. Extended period for resolution applicant

The amendment has also relieved the successful resolution applicant by granting a period of 1 year to pass all the legal hurdles and gain necessary approvals in accordance with the resolution plan. Earlier, there was no statutory period of fulfil the legal obligations.

Conclusion

The amendment would provide relief to many stakeholders of the Code - most importantly, the homebuyers of the real estate companies undergoing insolvency resolution process. These amendments will certainly result in increasing confidence of the lenders in the insolvency process and result in promoting resolution over liquidation of the companies.

Keeping the dictum and law as laid down in.. "Om Prakash V Reliance General Insurance And Anr." of the apex court, a bench of veena birbal madam and noor madam issued notice to reliance isurance company read more

Keeping the dictum and law as laid down in.. "Om Prakash V Reliance General Insurance And Anr." of the apex court, a bench of veena birbal madam and noor madam issued notice to reliance isurance company on a appeal filed by a botique hotel of south delhi though us. Feeling blessed and honored to represent one of the most reputed botique hotel of south delhi.

ACQUISITION OF SOLE PROPERTRSHIP CONCERN BY PRIVATE LIMITED COMPANY There is no such provisions given in Companies act 2013 to convert Sole proprietorship into Private Limited Company or take-over read more

ACQUISITION OF SOLE PROPERTRSHIP CONCERN

BY PRIVATE LIMITED

COMPANY

There is no such provisions given in Companies act 2013 to

convert Sole proprietorship into Private Limited Company or take-over of Sole

Proprietorship by Private Limited Company. You are running your proprietorship

firm which is not governed by any law. If you are filing Income tax return for

sole proprietorship firm and you want to grow your business, then it is good to

recommend you for converting it into Private Limited Company. Though there is

no specific provision given under Companies Act, 1956 and Companies Act, 2013

for conversion of Proprietorship firm into Private Limited Company, but as a

normal practice, the proprietorship firm being takeover by new Private Limited

Company. You can follow the procedure as stated below for converting sole

proprietorship business into Pvt. Ltd. company.

PROCEEDURE TO BE FOLLOWED BY PRIVATE

LIMITED COMPANY

1.Private

limited Company must contain object to take-over the sole proprietorship as

one of its main object in the Memorandum of Association. If it does not contain

the same in its object, the MoA has to be amended to insert the object.

2.The

Board of Director of the Private Company is required to take Board approval for

taking up the Sole proprietorship and later on required to pass Ordinary

resolution at EGM for approving the acquisition of Sole proprietorship.

3. Takeover Agreement/Sale agreement or deed of

assignment is required to be executed between Sole proprietorship and Private

company to transfer all its assets and liabilities. The Agreement shall specify

details of all the assets whether tangible or intangible which are required to

be transferred to the Company, it is up-to Owner of Sole proprietorship to

decide the category of assets it requires to sell and category of assets it

requires to keep for its personal use.

4.Debt

of Sole proprietorship cannot be transferred, so the owner can either settle

all the debts or it can take the consent of creditors to transfer the Sole

proprietorship to another Company.

5.Transfer

of Sole proprietorship to Company attracts Capital gain tax in the hands of

Owner of Sole proprietorship. Capital gain tax is required to be paid by the

Proprietor for transfer of assets. There are certain provision under section

47(xiv) in income tax act to avail the benefit of tax exemption on transfer of

assets from Sole proprietor to Company.

6.The

takeover is then done by submitting the agreement also known as contract and

other few documents like the company’s PAN card and certificate of

incorporation and return of allotment of shares if shares have been allotted to

the sole proprietor in consideration. These documents are submitted to the

Registrar of the Companies within 30 days of the completion of sale and

allotment of shares in consideration with prescribed fees. By completing this

process of taking over, all the assets and liabilities concerning the sole

proprietorship becomes the assets and liabilities of the company.

7.Further

attachments to this conversion would be the following;

·Affidavit

by the Sole Proprietor

·Statement

of Assets & Liabilities as on date by Chartered Accountant if the

proprietorship is doing business from long

·Income

Tax Returns Acknowledgement

·PAN

Card of the Sole Proprietor

·Sales

Tax Registration Number, if you have

·Any

other Proof showing the name of the Proprietorship firm

PROCEEDURE TO BE FOLLOWED BY SOLE

PROPRIETER

1.There

are certain procedure which has to be followed by Sole proprietor on

transferring the business to other Company. Owner has to inform the VAT

authorities and all the other authorities where it has been registered and has

to surrender all the registration certificate.

2.Final

income tax return till the date of transfer with previous return is required to

be submitted with clearing all the dues.

3.Acknowledgment

from VAT Authority and all other authorities wherever it has been registered

shall be taken.

4.All

the assets and liabilities shall be transferred to private company and all the

agreements and contracts in the name of Sole proprietorship shall be either

re-entered or rectified in the name of Company.

5.As

Debt and Liabilities of Sole proprietor is not transferred to other company, so

all the loans or debt has to be settled before it has been transferred to

private limited company or consent from creditors shall be taken and no new

bill is to be raised in the name of Sole Proprietorship.

6.The

Company cannot work with the bank account of Sole proprietorship so, it has to

close all the accounts in the name of Sole proprietorship and new account shall

be opened in the name of Company.

7.Further

TIN number and PAN number these are not transferred, so proprietor has to

surrender all the TIN and PAN etc. identity and has to apply for fresh TIN and

PAN and other registration in the name of Company.

8.Finally,

the proprietorship will then be needed to shut down officially. Use of any

licenses or tax registrations by the proprietorship can then be discontinued or

they can be surrendered to the authorities. That is the government should be

informed of the closing.

The process involves registering a whole company in case of

new company and then furnishing more documents in order to complete the

takeover and finally terminating the proprietorship.

Exemption under the

Income Tax Act:

Conversion of a sole proprietorship into a private limited

company entails a “transfer” within the meaning of the Income Tax Act, 1961, as

amended (Income Tax Act). That is, the assets of the sole proprietorship

concern are considered transferred to the newly formed company, which makes the

sole proprietor liable to pay tax for any capital gains calculated on such

transfer. However, there is a provision under section 47(xiv) of the income Tax

Act, which lays down certain conditions for exemption from any capital gains.

The conditions are:

·All

the assets and liabilities of the sole proprietary concern relating to the

business immediately before the succession become the assets and liabilities of

the company;

·The

shareholding of the sole proprietor in the company is not less than fifty per

cent (50%) of the total voting rights in the company and such shareholding

continues to so remain as such for a period of five years from the date of the

succession; and

·The

sole proprietor does not receive any consideration or benefit, directly or

indirectly, in any form or manner, other than by way of allotment of shares in

the company;

If any of the conditions laid down above are not complied

with (say the sole proprietor sells his share in two years instead of holding

on to the shareholding for five years), the amount of profits or gains arising

from the transfer of such capital assets or intangible assets not charged

earlier by virtue of these conditions, shall be deemed to be the profits and

gains chargeable to tax of the successor company for the previous year in which

the requirements are not complied with.

So therefore,

If you are a sole proprietor who intends to convert his sole

proprietorship into a private limited company, and also allot shares to

yourself, then it is imperative that an agreement is entered into for such

allotment and one of the conditions in the agreement should state that your

shareholding / voting rights will not fall below fifty per cent (50%) in the

next five years.

Facts related to

debt-

Debts of a sole proprietorship are actually debts of the

individual owner and are not transferable to a new owner. If the business has

debts that will not be paid in full prior to the transfer, discuss with the

creditor whether the new owner may assume the debt before agreeing to the sale

or transfer.

WHY SMALL & MEDIOCRE COMPANIES/ ENTREPRENEURS SHOULD ALWAYS HIRE A LAWYER ? Generally, the small or mediocre level companies or startups avoid hiring lawyers in order to save their cost and resources. read more

WHY SMALL & MEDIOCRE COMPANIES/ ENTREPRENEURS SHOULD ALWAYS HIRE A LAWYER ?

Generally, the small or mediocre level companies or startups avoid hiring lawyers in order to save their cost and resources. But let me make you aware that this decision can prove to be the worst decision ever for your company.

BENEFITS OF HIRING A BUSINESS LAWYER ?

1- Protection from fraudulent motives/ intentions of third party such as dealers/ buyers/ partners/ agents etc.

2- Managing the employees and their legal issues. And then sue those employees for damages they have made to company by non performance.

3- Anticipation of Legal consequences for company.

4- Advising in each step and analyzing the legal issues/ dispute that may arise in future and tackling those issues at earlier stages only so that anything adverse do not happen.

5- Recovering the money legally from cheaters and fraud people.

6- Drafting and reviewing all the documents so that any clause may not harm company in future.

It is not wrong to say that lawyers act as a protecting shield for the company.

Thus, hire your business lawyer now because there is no app or software to replace a business lawyer and google is not going to help you for long :)

Clearly describing Personal Body Safety rules involves helping children develop the capacity to recognize, resist (to the extent possible) and report sexual abuse.Through one’s experience, Enfold has read more

Clearly describing Personal Body Safety rules involves helping children develop the capacity to recognize, resist (to the extent possible) and report sexual abuse.Through one’s experience, Enfold has often come across individuals who communicate the Touching Rule using the words “good and bad”, when helping children learn personal safety rules.

Enfold prefers to use the terms Safe Touch and Unsafe Touch instead of Good Touch and Bad Touch. Our rationale:

Good and bad are moralistic, judgmental words.

Good: noun – that which is morally right; righteousness. Adjective – to be desired or approved of.

Bad: adjective – of poor quality or a low standard., not such as to be hoped for or desired; unpleasant or unwelcome.

Safe: Adjective – not likely to cause or lead to harm or injury; not involving danger or risk.

Unsafe: Adjective – dangerous, risky, insecure

It is easier to explain the concept of safety to a child than untangle the morality of people’s actions or how one is feeling.

While explaining personal safety rules about clothing, touching and talking, link them to traffic rules. The concept of safe and unsafe driving can be used to talk about people who deliberately break personal safety rules for their own benefit – at the expense of others – like people who jump a red light to save their time but hurt others in the process. This also helps shift the blame from the survivor to the perpetrator, thereby increasing the chances of reporting.

We attach emotions to every word we use. Good and bad are loaded with feelings of acceptance, righteousness at one end to feelings of rejection, guilt and stigma at the other end. Children may transfer the ‘badness of a bad touch to themselves and assume that they have become bad in the process – especially since the touch involves parts of the body that people seem to consider dirty/ sinful or bad anyway.

Safe and unsafe carry emotions of security, confidence at one end to caution and danger at the other end. These emotions can be used to help children report abusers.

“Good boy” “Bad boy” are adjectives our children hear day in and day out. They are used to make a child feel good or bad about themselves, and carry a promise of a reward or a threat of punishment. In such a scenario, a child is unlikely to report ‘bad touch’. He/she may find it easier to report an unsafe touch, since safe and unsafe are emotionally less loaded words and specify that the behaviour of the perpetrator was unsafe.

Given the nature and function of the sexual organs, a bad touch can sometimes feel good, thereby confusing the child. This confusion increases when children grow up and begin to explore their sexuality further or when they enter an intimate, sexual relationship. Besides hindering a healthy sexual life, it also runs the risk of transferring the discomfort and secrecy around reproductive health and personal safety to the next generation.

Enfold suggests the use of the words safe and unsafe touch, instead of good and bad touch to avoid confusion and fear in the minds of children, especially with their bodies. This will need to be accompanied with answering our growing child’s questions using simple words that address and explain the doubt in the child/ adolescent’s mind in a respectful and scientific manner. This will hopefully create an environment which has healthy and safe children living with dignity supported by empowered adults.

As we all know that Government is insisting to move towards digitization, be it in any sector whether it is Financial, Education or even for that matter Agriculture. Government has also asked to bring read more

As we all know that Government is insisting to move towards digitization, be it in any sector whether it is Financial, Education or even for that matter Agriculture. Government has also asked to bring to their notice the issues being faced by general public so that genuine reforms can be initiated.

IntroductionLabour laws in India are vast and expansive. Sometimes, a term has different meanings and interpretations under different legislation. For example, even a basic yet most important term ‘wages’ read more

Introduction

Labour laws in India

are vast and expansive. Sometimes, a term has different meanings and

interpretations under different legislation. For example, even a basic yet most

important term ‘wages’ is defined differently in many labour enactments.

This has led to immense

confusion in the applicability of labour laws. Labour law experts have time and

again emphasised the need to ensure uniformity in labour laws. The Government,

in pursuance of such recommendations, introduced the Code on Wages Bill, 2017

(“Code on Wages”) in August, 2017 in the Lok Sabha.

This Bill proposes to

consolidate four existing laws namely, Payment of Wages Act, Payment of Bonus

Act, Minimum Wages Act and Equal Remuneration Act. We have discussed and

analysed the key features of the Code on Wages in the present article.

Key

Features of the Code on Wages

Changes to Minimum

Wages

ØMinimum

Wages now to be applicable to all types of employment: Under the extant

minimum wage legislation, certain employments are notified as scheduled

employments and only the persons employed in such employment are entitled to

minimum wages. This leads to exclusion of a large amount of workforce,

especially those employed in the unorganised sector.

The

Code on Wages would dispense away with the system of applying minimum wages

only to scheduled employments and would bring all employment within the ambit

of minimum wages.

Hence,

under the Code on Wages, persons employed in all kinds of employments including

the unorganised sector would be entitled to a minimum wage.

ØNational

Minimum Wage:The

Code on Wages has proposed the formulation of a National Minimum Wage by the

Centre. Unlike its nomenclature, a National Minimum Wage does not mean a

uniform minimum wage across the country.

A

National Minimum Wage would be a baseline wage fixed by the centre. It may be

different for different regions. States would be compelled to fix their

respective minimum wages, either equal to or above such National Minimum Wage.

ØA

fixed time period of five years has been set for wage revision. Earlier, the

state governments were free to revise the minimum wages at any point of time,

as long as it did not exceed a period of five years.

Provisions relating to

Equal Remuneration

The Code on

Wages would also subsume the Equal Remuneration Act, 1976. While it mandates no

discrimination in payment of wages, the provisions pertaining to no

discrimination at the time of recruitment are absent from the Code.

The maximum penalty

under the Code on Wages has been fixed as three months imprisonment and a fine up to INR 1

Lakh.

Analysis

of the Code on Wages

While the intent to proposing

a uniform code which would deal with payment of wages, minimum wages, bonus and

equal remuneration all by itself is a laudable move, there are still certain

creases which need to be straightened before this Code can be implemented.

Firstly, the proposal

of introducing a national minimum wage which may vary regionally can cause

confusion among the stakeholders. It is better, if the centre releases

guidelines for a base minimum wage and the States follow the same, rather than

introducing the concept of a national minimum wage.

Secondly, fixing the

time period for revision of wages as five years may not be the best thing to

do. Earlier system provided the State governments with flexibility to revise

their minimum wages. The only condition imposed was to do so within a time span

of five years. Such flexibility should remain under the new system as well.

Thirdly, the Code on

Wages is silent with respect to provisions prohibiting gender discrimination at

the time of recruitment. This is an essential provision which cannot be omitted

from the Code on Wages.

Having discussed only

some of the existing loopholes in the Code on Wages Bill, it is pertinent to

state that, despite such flaws, the Code on Wages would go a long way in

creating more definitiveness in the Indian labour law jurisprudence and infuse

more confidence in all quarters.

In the social jungle of human existence, there is no feeling of being alive without a sense of identity. ~Erik EriksonPermanent Account Number is a 10 digit alphanumeric number issued by the read more

In the social jungle of human existence, there is no feeling of being alive without a sense of identity. ~Erik Erikson

Permanent Account Number is a 10 digit alphanumeric numberissued by the Income Tax Authorities under the supervision of Central Board of Direct Taxes or CBDT.

It is a unique number assignedto an individual and is mandatory from taxation point of view and every individual should have one. The primary motive and purpose of a PAN card is to track the financial transactions carried out by individuals so as to keep tabs on any illegal money laundering and also to avoid tax evasion. However apart from filling your taxes and giving details of your financial transactions, PAN is required for a number of other reasons as well.

In a layman’s language the simple use of this card is why to keep so many documents and records in paper which might get lost when all your information is stored in a single card which if may get lost there won’t be any misuse because it is your permanent number which will remain alive as a proof even after your death. It’s just not an account number but it proves the nationality of an individual which may help in times if any trouble occurs in future. If we are trying to succeed ourself in the race of globalization as well as digitalization why not to consider these small things which might prove as a very helpful instrument to the citizens as well to the nation too.

It’s not very difficult to get a PAN card, one can get the form from the various offices present n different cities and even by online process where your PAN car will be posted directly at your doorstep after the verification of your documents though charges may differ if you are applying for it online. It seems to be very useful when you are It is necessary to give the PAN card number when you buy or sell immovable properties in India,when you buy automobiles, you will have to give this number, buying banker’s draft, pay orders and checks require PAN card, if you buy shares or debentures exceeding the value of Rs. 1 lakh, you need to supply the PAN card, PAN card is necessary to make any deposit exceeding Rs. 50000.00,PAN card is also necessary for initiating a bank account, starting a demat account or applying for a credit card and finally, you may produce the PAN card as a valid photo ID proof. The advantages of keeping PAN card are Without a PAN card, you will be taxed at the highest rate possible,If you pay TDS (tax deducted at source), that cannot be counted without a PAN card and you may end up paying tax twice,with a valid PAN card, you can easily enter into different financial transactions. You can obtain landline and cell phone connection; you can open demat account; you can buy and sell property and share and much more,If you are NRI, you can easily buy property or engage in business in India with the help of your PAN card without filing tax returns,a minor account can be opened and operated easily with the PAN card of the guardian,Not only does the PAN have all these great advantages, but also it is necessary to carry on most of the normal transactions. The process has been highly simplified. So, you should make no delay in getting your PAN card.

In adherence to the rules and regulations of Bar Council of India, this website has been

designed only for the purposes of circulation of information and not for the purpose of

advertising.

Your use of SoOLEGAL service is completely at your own risk. Readers and Subscribers

should seek proper advice from an expert before acting on the information mentioned

herein. The content on this website is general information and none of the information

contained on the website is in the nature of a legal opinion or otherwise amounts to any

legal advice. User is requested to use his or her judgment and exchange of any such

information shall be solely at the user’s risk.

SoOLEGAL does not take responsibility for actions of any member registered on the site

and is not accountable for any decision taken by the reader on the basis of

information/commitment provided by the registered member(s).By clicking on ‘ENTER’,

the visitor acknowledges that the information provided in the website (a) does not

amount to advertising or solicitation and (b) is meant only for his/her understanding

about our activities and who we are.

Sign up for SoOLEGAL mobile app

Launching on 10th Jan 2017

Members

Client Services

Search in Legal Resource

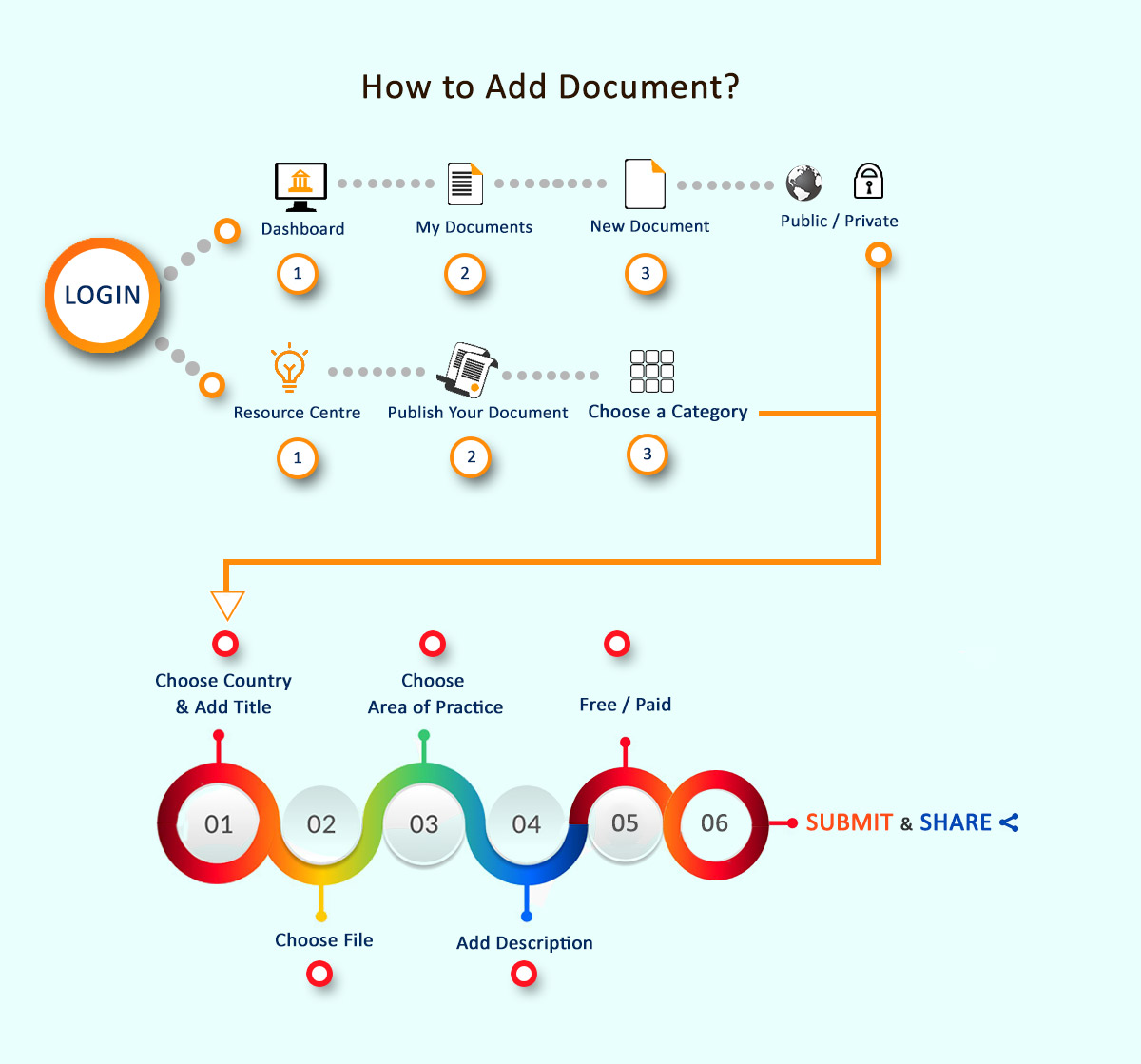

Resource centre is one stop destination for users who are seeking for latest updates and information related to the law. takes the privilege to bring every single legal resource to your knowledge in a hassle free way. Legal Content in resource centre to help you understand your case, legal requirements. More than 3000 Documents are available for Reading and Download which are listed in below categories:

Legal documents - Legal Drafts, Forms, Affidavits, Pleadings, Deeds etc.

By

registering yourself with SoOLEGAL, it is understood and agreed by

you that the Terms and Conditions under the Transaction Services

Terms shall be binding on you at all times during the period of

registration and notwithstanding cessation of your registration with

SoOLEGAL certain Terms and Conditions shall survive.

"Your

Transaction" means any Transaction of Documents/

Advices(s), advice and/ or solution in the form of any written

communication to your Client made by you arising out of any advice/

solution sought from you through the SoOLEGAL Site.

Transacting

on SoOLEGAL Service Terms:

The

SoOLEGAL Payment

System Service

("Transacting on SoOLEGAL") is a Service that allows you to

list Documents/ Advices which comprise of advice/ solution in the

form of written communication to your Client who seeks your advice/

solution via SoOLEGAL Site and such Documents/ Advices being for

Transaction directly via the SoOLEGAL Site. SoOLEGAL

Payment Service

is operated by Sun Integrated Technologies and Applications .

TheSoOLEGAL

Payment System

Service Terms are part of the Terms & Conditions

of SoOLEGAL Services Transaction Terms and Conditionsbut unless

specifically provided otherwise, concern and apply only to your

participation in Transacting on SoOLEGAL. BY REGISTERING FOR OR USING

SoOLEGAL

PAYMENT SYSTEM ,

YOU (ON BEHALF OF YOURSELF OR THE FIRM YOU REPRESENT) AGREE TO BE

BOUND BY THE TRANSACTIONS TRANSACTION TERMS AND CONDITIONS.

Unless

otherwise defined in this Documents/ Advice or Terms & Conditions

which being the guiding Documents/ Advice to this Documents/ Advice,

all capitalized terms have the meanings given them in the

Transactions Transaction Terms and Conditions.

S-1.

Your Documents/ Advice Listings and Orders

S-1.1

Documents/ Advices

Information. You

will, in accordance with applicable Program Policies, provide in the

format we require. Documents/ Advices intended to be sold should be

accurate and complete and thereafter posted through the SoOLEGAL

Site and promptly update such information as necessary to ensure it

at all times that such Documents/ Advices remain accurate and

complete. You will also ensure that Your Materials, Your Documents/

Advices (including comments) and your offer and subsequent

Transaction of any ancillary Documents/ Advice pertaining to the

previous Documents/ Advices on the SoOLEGAL Site comply with all

applicable Laws (including all marking and labeling

requirements) and do not contain any sexually explicit, defamatory or

obscene materials or any unlawful materials. You may not provide any

information for, or otherwise seek to list for Transaction on the

SoOLEGAL Site, any Excluded Documents/ Advices; or provide any URL

Marks for use, or request that any URL Marks be used, on the SoOLEGAL

Site. In any event of unlawful Documents/ Advices made available for

Transaction by you on SoOLEGAL site, it is understood that

liabilities limited or unlimited shall be yours exclusively to which

SoOLEGAL officers, administrators, Affiliates among other authorized

personnel shall not be held responsible and you shall be liable to

appropriate action under applicable laws.

S-1.2

Documents/ Advices Listing; Merchandising; Order Processing. We

will list Your Documents/ Advices for Transaction on the SoOLEGAL

Site in the applicable Documents/ Advices categories which are

supported for third party REGISTERED USERs generally on the SoOLEGAL

Site on the applicable Transacting Associated Properties or any other

functions, features, advertising, or programs on or in connection

with the SoOLEGAL Site). SoOLEGAL reserves its right to restrict at

any time in its sole discretion the access to list in any or all

categories on the SoOLEGAL Site. We may use mechanisms that rate, or

allow users to rate, Your Documents/ Advices and/or your performance

as a REGISTERED USER on the SoOLEGAL Site and SoOLEGAL may make these

ratings and feedback publicly available. We will provide Order

Information to you for each of Your Transactions. Transactions

Proceeds will be paid to you only in accordance with Section S-6.

S-1.3

a. It is mandatory to secure an advance amount from Client where

SoOLEGAL Registered Consultant will raise an invoice asking for a 25%

advance payment for the work that is committed to be performed for

the Client of such SoOLEGAL Registered Consultant. The amount will be

refunded to the client if the work is not done and uploaded to

SoOLEGAL Repository within the stipulated timeline stated by SoOLEGAL

Registered Consultant.

b.

SoOLEGAL Consultant will be informed immediately on receipt of

advance payment from Client which will be held by SoOLegal and will

not be released to either Party and an email requesting the

Registered Consultant will be sent to initiate the assignment.

c.

The Registered Consultant will be asked on the timeline for

completion of the assignment which will be intimated to Client.

d.

Once the work is completed by the consultant the document/ advice

note will be in SoOLEGAL

repository and once Client makes rest of the payment, the full amount

will be remitted to the consultant in the next payment cycle and the

document access will be given to the client.

e.

In the event where the Client fails to make payment of the balance

amount

within 30 days from the date of upload ,

the Registered Consultant shall receive

the advance amount paid by the Client without any interest in the

next time cycle

after the lapse of 30 days.

S-1.4

Credit Card Fraud.

We

will not bear the risk of credit card fraud (i.e. a fraudulent

purchase arising from the theft and unauthorised

use of a third party's credit card information) occurring in

connection with Your Transactions. We may in our sole discretion

withhold for investigation, refuse to process, restrict download for,

stop and/or cancel any of Your Transactions. You will stop and/or

cancel orders of Your Documents/ Advices if we ask you to do so. You

will refund any customer (in accordance with Section

S-2.2)

that has been charged for an order that we stop or cancel.

S-2.

Transaction and Fulfilment, Refunds and Returns

S-2.1

Transaction and Fulfilment:

Fulfilment

– Fulfilment is categorised under the following heads:

1.

Fulfilment by Registered User/ Consultant - In the event of Client

seeking consultation, Registered User/ Consultant

has

to ensure the quality of the product and as per the requirement of

the Client and if its not as per client, it will not be SoOLEGAL’s

responsibility and it will be assumed

that the Registered User/ Consultant and the Client have had

correspondence before assigning the work to the Registered User/

Consultant.

2.

Fulfilment by SoOLEGAL - If the Registered User/ Consultant has

uploaded the Documents/ Advice in SoOLEGAL Site, SoOLEGAL Authorised

personnel does not access such Documents/ Advice and privacy of the

Client’s Documents/ Advice and information is confidential and will

be encrypted and upon payment by Client, the Documents/ Advice is

emailed by SoOLEGAL to them. Client’s information including email

id will be furnished to SoOLEGAL by Registered User/ Consultant.

If

Documents/ Advice is not sent to Client, SoOLEGAL will refund any

amount paid to such Client’s account without interest within 60

days.

3.

SoOLEGAL will charge 5% of the transaction value which is subject to

change with time due to various economic and financial factors

including inflation among other things, which will be as per

SoOLEGAL’s discretion

and will be informed to Registered Users about the same from time to

time. Any tax applicable on Registered User/ Consultant is payable by

such Registered User/ Consultant and not by SoOLEGAL.

4.

SoOLEGAL will remit the fees (without any interest) to its Registered

User/ Consultant every 15 (fifteen) days. If there is any discrepancy

in such payment, it should be reported to Accounts Head of SoOLEGAL

(accounts@soolegal.com) with all relevant account statement within

fifteen days from receipt of that last cycle payment. Any discrepancy

will be addressed in the next fifteen days cycle. If any discrepancy

is not reported within 15 days of receipt of payment, such payment

shall be deemed accepted and SoOLEGAL shall not entertain any such

reports thereafter.

5.

Any Registered User/ Consultant wishes to discontinue with this, such

Registered User/ Consultant shall send email to SoOLEGAL and such

account will be closed and all credits will be refunded to such

Registered User/ Consultant after deducation of all taxes and

applicable fees within 30 days. Other than as described in the

Fulfilment by SoOLEGAL Terms & Conditions (if applicable to you),

for the SoOLEGAL Site for which you register or use the Transacting

on SoOLEGAL Service, you will: (a) source, fulfil and transact with

your Documents/ Advices, in each case in accordance with the terms of

the applicable Order Information, these Transaction Terms &

Conditions, and all terms provided by you and displayed on the

SoOLEGAL Site at the time of the order and be solely responsible for

and bear all risk for such activities; (a) not cancel any of Your

Transactions except as may be permitted pursuant to your Terms &

Conditions appearing on the SoOLEGAL Site at the time of the

applicable order (which Terms & Conditions will be in accordance

with Transaction Terms & Conditions) or as may be required

Transaction Terms & Conditions

per

the terms laid in this Documents/ Advice; in each case as requested

by us using the processes designated by us, and we may make any of

this information publicly available notwithstanding any other

provision of the Terms mentioned herein, ensure that you are the

REGISTERED USER of all Documents/ Advices made available for listing

for Transaction hereunder; identify yourself as the REGISTERED USER

of the Documents/ Advices on all downloads or other information

included with Your Documents/ Advices and as the Person to which a

customer may return the applicable Documents/ Advices; and

S-2.2

Returns and Refunds. For

all of Your Documents/ Advices that are not fulfilled using

Fulfilment by SoOLEGAL, you will accept and process returns, refunds

and adjustments in accordance with these Transaction Terms &

Conditions and the SoOLEGAL Refund Policies published at the time of

the applicable order, and we may inform customers that these policies

apply to Your Documents/ Advices. You will determine and calculate

the amount of all refunds and adjustments (including any taxes,

shipping of any hard copy and handling or other charges) or other

amounts to be paid by you to customers in connection with Your

Transactions, using a functionality we enable for Your Account. This

functionality may be modified or discontinued by us at any time

without notice and is subject to the Program Policies and the terms

of thisTransaction Terms & Conditions Documents/ Advice. You will

route all such payments through SoOLEGAL We will provide any such

payments to the customer (which may be in the same payment form

originally used to purchase Your Documents/ Advices), and you will

reimburse us for all amounts so paid. For all of Your Documents/

Advices that are fulfilled using Fulfilment by SoOLEGAL, the SoOLEGAL

Refund Policies published at the time of the applicable order will

apply and you will comply with them. You will promptly provide

refunds and adjustments that you are obligated to provide under the

applicable SoOLEGAL Refund Policies and as required by Law, and in no

case later than thirty (30) calendar days following after the

obligation arises. For the purposes of making payments to the

customer (which may be in the same payment form originally used to

purchase Your Documents/ Advices), you authorize us to make such

payments or disbursements from your available balance in the Nodal

Account (as defined in Section S-6). In the event your balance in the

Nodal Account is insufficient to process the refund request, we will

process such amounts due to the customer on your behalf, and you will

reimburse us for all such amount so paid.

S-5.

Compensation

You

will pay us: (a) the applicable Referral Fee; (b) any applicable

Closing Fees; and (c) if applicable, the non-refundable Transacting

on SoOLEGAL Subscription Fee in advance for each month (or for each

transaction, if applicable) during the Term of this Transaction Terms

& Conditions. "Transacting on SoOLEGAL Subscription Fee"

means the fee specified as such on the Transacting

on SoOLEGALSoOLEGAL Fee Schedule for the SoOLEGAL Site at

the time such fee is payable. With respect to each of Your

Transactions: (x) "Transactions Proceeds" has the

meaning set out in the Transaction Terms & Conditions;

(y) "Closing Fees" means the applicable fee, if

any, as specified in the Transacting

on SoOLEGAL Fee Schedule for the SoOLEGAL Site; and

(z) "Referral

Fee" means

the applicable percentage of the Transactions Proceeds from Your

Transaction through the SoOLEGAL Site specified on the Transacting

on SoOLEGAL Fee Schedule for the SoOLEGAL Site at the time

of Your Transaction, based on the categorization by SoOLEGAL of the

type of Documents/ Advices that is the subject of Your Transaction;

provided, however, that Transactions Proceeds will not include any

shipping charge set by us in the case of Your Transactions that

consist solely of SoOLEGAL-Fulfilled Documents/ Advices. Except as

provided otherwise, all monetary amounts contemplated in these

Service Terms will be expressed and provided in the Local Currency,

and all payments contemplated by this Transaction Terms &

Conditions will be made in the Local Currency.

All

taxes or surcharges imposed on fees payable by you to SoOLEGAL will

be your responsibility.

S-6

Transactions Proceeds & Refunds.

S-6.1.Nodal

Account.Remittances

to you for Your Transactions will be made through a nodal account

(the "Nodal Account") in accordance with the directions

issued by Reserve Bank of India for the opening and operation of

accounts and settlement of payments for electronic payment

transactions involving intermediaries vide its notification

RBI/2009-10/231 DPSS.CO.PD.No.1102 / 02.14.08/ 2009-10 dated November

24, 2009. You hereby agree and authorize us to collect payments on

your behalf from customers for any Transactions. You authorize and

permit us to collect and disclose any information (which may include

personal or sensitive information such as Your Bank Account

information) made available to us in connection with the Transaction

Terms & Conditions mentioned hereunder to a bank, auditor,

processing agency, or third party contracted by us in connection with

this Transaction Terms & Conditions.

Subject

to and without limiting any of the rights described in Section 2 of

the General Terms, we may hold back a portion or your Transaction

Proceeds as a separate reserve ("Reserve").

The Reserve will be in an amount as determined by us and the Reserve

will be used only for the purpose of settling the future claims of

customers in the event of non-fulfillment of delivery to the

customers of your Documents/ Advices keeping in mind the period for

refunds and chargebacks.

S-6.2. Except

as otherwise stated in this Transaction Terms & Conditions

Documents/ Advice (including without limitation Section 2 of the

General Terms), you authorize us and we will remit the Settlement

Amount to Your Bank Account on the Payment Date in respect of an

Eligible Transaction. When you either initially provide or later

change Your Bank Account information, the Payment Date will be

deferred for a period of up to 14 calendar days. You will not have

the ability to initiate or cause payments to be made to you. If you

refund money to a customer in connection with one of Your

Transactions in accordance with Section S-2.2, on the next available

Designated Day for SoOLEGAL Site, we will credit you with the amount

to us attributable to the amount of the customer refund, less the

Refund Administration Fee for each refund, which amount we may retain

as an administrative fee.

"Eligible

Transaction"

means Your Transaction against which the actual shipment date has

been confirmed by you.

"Designated

Day" means any particular Day of the week designated by SoOLEGAL

on a weekly basis, in its sole discretion, for making remittances to

you.

"Payment

Date" means the Designated Day falling immediately after 14

calendar days (or less in our sole discretion) of the Eligible

Transaction.

"Settlement

Amount" means Invoices raised through SoOLEGAL Platform (which

you will accept as payment in full for the Transaction and shipping

and handling of Your Documents/ Advices), less: (a) the Referral Fees

due for such sums; (b) any Transacting on SoOLEGAL Subscription Fees

due; (c) taxes required to be charged by us on our fees; (d) any

refunds due to customers in connection with the SoOLEGAL Site; (e)

Reserves, as may be applicable, as per this Transaction Terms &

Conditions; (f) Closing Fees, if applicable; and (g) any other

applicable fee prescribed under the Program Policies. SoOLEGAL shall

not be responsible for

S-6.3. In

the event that we elect not to recover from you a customer's

chargeback, failed payment, or other payment reversal (a "Payment

Failure"), you irrevocably assign to us all your rights, title

and interest in and associated with that Payment Failure.

S-7.

Control of Site

Notwithstanding

any provision of this Transaction Terms & Conditions, we will

have the right in our sole discretion to determine the content,

appearance, design, functionality and all other aspects of the

SoOLEGAL Site and the Transacting on SoOLEGAL Service (including the

right to re-design, modify, remove and alter the content, appearance,

design, functionality, and other aspects of, and prevent or restrict

access to any of the SoOLEGAL Site and the Transacting on SoOLEGAL

Service and any element, aspect, portion or feature thereof

(including any listings), from time to time) and to delay or suspend

listing of, or to refuse to list, or to de-list, or require you not

to list any or all Documents/ Advices on the SoOLEGAL Site in our

sole discretion.

S-8.

Effect of Termination

Upon

termination of this Contract, the Transaction Terms & Conditions

automatiocally stands terminated and in connection with the SoOLEGAL

Site, all rights and obligations of the parties under these Service

Terms with regard to the SoOLEGAL Site will be extinguished, except

that the rights and obligations of the parties with respect to Your

Transactions occurring during the Term will survive the termination

or expiration of the Term.

"SoOLEGAL

Refund Policies" means

the return and refund policies published on the SoOLEGAL Site.

"Required

Documents/ Advices Information"means,

with respect to each of Your Documents/ Advices in connection with

the SoOLEGAL Site, the following (except to the extent expressly not

required under the applicable Policies) categorization within each

SoOLEGAL Documents/ Advices category and browse structure as

prescribed by SoOLEGAL from time to time, Purchase Price; Documents/

Advice Usage, any text, disclaimers, warnings, notices, labels or

other content required by applicable Law to be displayed in

connection with the offer, merchandising, advertising or Transaction

of Your Documents/ Advices, requirements, fees or other terms and

conditions applicable to such Documents/ Advices that a customer

should be aware of prior to purchasing the Documents/ Advices;

"Transacting

on SoOLEGAL Launch Date"means

the date on which we first list one of Your Documents/ Advices for

Transaction on the SoOLEGAL Site.

"URL

Marks" means

any Trademark, or any other logo, name, phrase, identifier or

character string, that contains or incorporates any top level domain

(e.g., .com, co.in, co.uk, .in, .de, .es, .edu, .fr, .jp) or any

variation thereof (e.g., dot com, dotcom, net, or com).

"Your

Transaction"is

defined in the Transaction Terms & Conditions; however, as used

in Terms & Conditions, it shall mean any and all such

transactions whereby you conduct Transacting of Documents/ Advices or

advice sought from you by clients/ customers in writing or by any

other mode which is in coherence with SoOLEGAL policy on SoOLEGAL

site only.

Taxes

on Fees Payable to SoOLEGAL.In

regard to these Service Terms you can provide a PAN registration

number or any other Registration/ Enrolment number that reflects your

Professional capacity by virtue of various enactments in place. If

you are PAN registered, or any professional Firm but not PAN

registered, you give the following warranties and representations:

(a)

all services provided by SoOLEGAL to you are being received by your

establishment under your designated PAN registration number; and

SoOLEGAL

reserves the right to request additional information and to confirm

the validity of any your account information (including without

limitation your PAN registration number) from you or government

authorities and agencies as permitted by Law and you hereby

irrevocably authorize SoOLEGAL to request and obtain such information

from such government authorities and agencies. Further, you agree to

provide any such information to SoOLEGAL upon request. SoOLEGAL

reserves the right to charge you any applicable unbilled PAN if you

provide a PAN registration number, or evidence of being in a

Professional Firm, that is determined to be invalid. PAN registered

REGISTERED USERs and REGISTERED USERs who provide evidence of being

in Law Firm agree to accept electronic PAN invoices in a format and

method of delivery as determined by SoOLEGAL.

All

payments by SoOLEGAL to you shall be made subject to any applicable

withholding taxes under the applicable Law. SoOLEGAL will retain, in

addition to its net Fees, an amount equal to the legally applicable

withholding taxes at the applicable rate. You are responsible for

deducting and depositing the legally applicable taxes and deliver to

SoOLEGAL sufficient Documents/ Advice evidencing the deposit of tax.

Upon receipt of the evidence of deduction of tax, SoOLEGAL will remit

the amount evidenced in the certificate to you. Upon your failure to

duly deposit these taxes and providing evidence to that effect within

5 days from the end of the relevant month, SoOLEGAL shall have the

right to utilize the retained amount for discharging its tax

liability.

Where

you have deposited the taxes, you will issue an appropriate tax

withholding certificate for such amount to SoOLEGAL and SoOLEGAL

shall provide necessary support and Documents/ Adviceation as may be

required by you for discharging your obligations.

SoOLEGAL

has the option to obtain an order for lower or NIL withholding tax

from the Indian Revenue authorities. In case SoOLEGAL successfully

procures such an order, it will communicate the same to you. In that

case, the amounts retained, shall be in accordance with the

directions contained in the order as in force at the point in time

when tax is required to be deducted at source.

Any

taxes applicable in addition to the fee payable to SoOLEGAL shall be

added to the invoiced amount as per applicable Law at the invoicing

date which shall be paid by you.F.11.

Indemnity

Category

and Documents/ Advice Restrictions

Certain

Documents/ Advices cannot be listed or sold on SoOLEGAL site as a

matter of compliance with legal or regulatory restrictions (for

example, prescription drugs) or in accordance with SoOLEGAL

policy (for example, crime scene photos).

SoOLEGAL's

policies also prohibit specific types of Documents/ Advice

content. For guidelines on prohibited content and copyright

violations, see our Prohibited

Content list.

For

some Documents/ Advice categories, REGISTERED USERS may not create

Documents/ Advice listings without prior approval from SoOLEGAL.

In

addition to your obligations under Section

6 of

the Transaction Terms & Conditions, you also agree to indemnify,

defend and hold harmless us, our Affiliates and their and our

respective officers, directors, employees, representatives and agents

against any Claim that arises out of or relates to: (a) the Units

(whether or not title has transferred to us, and including any Unit

that we identify as yours pursuant to Section

F-4 regardless

of whether such Unit is the actual item you originally sent to us),

including any personal injury, death or property damage; and b) any

of Your Taxes or the collection, payment or failure to collect or pay

Your Taxes.

Registered

Users must at all times adhere to the following rules for the

Documents/ Advices they intend to put on Transaction:

The

"Add a Documents/ Advice" feature allows REGISTERED USERS

to create Documents/ Advice details pages for Documents/ Advices.

The

following rules and restrictions apply to REGISTERED USERS who use

the SoOLEGAL.in "Add a Documents/ Advice" feature.

Using

this feature for any purpose other than creating Documents/ Advice

details pages is prohibited.

Any

Documents/ Advice already in the SoOLEGAL.in catalogue which is not

novel and/ or unique or has already been provided by any other

Registered User which may give rise to Intellectual Property

infringement of any other Registered User is prohibited.

Detail

pages may not feature or contain Prohibited

Contentor.

The

inclusion of any of the following information in detail page titles,

descriptions, bullet points, or images is prohibited:

Information

which is grossly harmful, harassing, blasphemous, defamatory,

pedophilic, libelous, invasive of another's privacy, hateful, or

racially, ethnically objectionable, disparaging, relating or

encouraging money laundering or gambling, pornographic, obscene or

offensive content or otherwise unlawful in any manner whatever.

Availability,

price, condition, alternative ordering information (such as links to

other websites for placing orders).

Reviews,

quotes or testimonials.

Solicitations

for positive customer reviews.

Advertisements,

promotional material, or watermarks on images, photos or videos.

Time-sensitive

information

Information

which belongs to another person and to which the REGISTERED USER

does not have any right to.

Information

which infringes any patent, trademark, copyright or other

proprietary rights.

Information

which deceives or misleads the addressee about the origin of the

messages or communicates any information which is grossly offensive

or menacing in nature.

Information

which threatens the unity, integrity, defence, security or

sovereignty of India, friendly relations with foreign states, or

public order or causes incitement to the commission of any

cognizable offence or prevents investigation of any offence or is

insulting any other nation.

Information

containing software viruses or any other computer code, files or

programs designed to interrupt, destroy or limit the functionality

of any computer resource.

Information

violating any law for the time being in force.

All

Documents/ Advices should be appropriately and accurately classified

to the most specific location available. Incorrectly classifying

Documents/ Advices is prohibited.

Documents/

Advice titles, Documents/ Advice descriptions, and bullets must be

clearly written and should assist the customer in understanding the

Documents/ Advice. .

All

Documents/ Advice images must meet SoOLEGAL general standards as